The Energy Information Administration released their weekly report on Thursday.

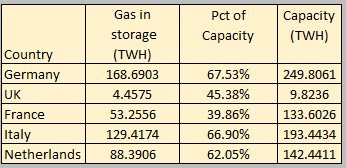

Nationally, inventories are well above the 5 year average, although still well below in the Pacific region. substantial gains have taken place over the past few weeks, having increased 27% in the past two weeks.

Pricing in the Pacific region did increase, but still remains within reach of other regions... which continue to be on the low side.

EU and UK continue to fare well, regarding inventories and remain well above both last year and seasonal 5 year averages.

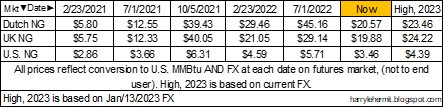

While pricing in Europe has fallen, it continues to be extremely high, compared to pre-covid and pre-invasion.

An example would be the U.K., where the price range is currently £1,509~£2,264. I compare that to the extreme predictions of £3,600~£5,400 from about 21 months ago, and the price cap rollout of £2,500.

The good news is the £2,500 cap will stay into June. I would think the cap could be lowered, based on current market pricing, but that is just my silly opinion. It's not like there is a large storage of higher priced natgas to work through, for th UK.

{kind=link}