It's been awhile since posting, although I never really stopped tracking.

Current U.S. inventories, compared to last week and 1 year ago.

Not terribly tight and I really don't see a significant drop off in U.S. consumer purchasing at the pump. Distillate exports reached an all time high during this reporting period. Additionally, the distillate inventory has dropped to levels not seen since 5/23/2003.

Pump prices compared to days gone by, factoring in inflation...

That $4.114 in July, 2008 is comparable to $6.176 in today's dollars. Also, the $5.016 of June, 2022 is comparable to $5.590 in today's dollars.

The market does seem to be settling down a bit, but I suspect that is more fear of getting caught over bought, due to some very clear demand destruction in Asia. Much was made if that 470M Barrels being released from various strategic petroleum reserves, but that is a drop in the bucket to the near 1B barrels that have been lost to the strait of hormuz blockade, etc.

Even if the blockade suddenly stopped tomorrow and the full complement of crude starts tomorrow... another 500M barrels will be removed from the global inventories, due to transit times of delivey. If you are keeping track... that is 1B barrels above the SPR release.

That demand destruction is taking place, is undeniable. Even with significant demand destruction of 5M barrels per day... it would take 6 months for a full recovery, imho.

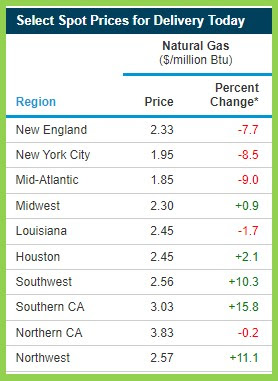

What I find interesting, is the lack of discussion of the current state of natural gas supplies. Qatar suffered a severe setback in its LNG liquefaction facilities. It will take some time to resolve that situation and while there are new Liquefaction facilities coming on line later this year... the current state of the European Union's Natural Gas storage if behind last year, with draws still above last year.

Purchases of Natural Gas for storage is woefully behind last year. Perhaps they see a milder winter coming up over the next 12 months. I guess what I am hinting at... Natural Gas prices in Europe are set to dramatically escalate in the coming months, OR... they may decide to swallow some pride and get some of that pipeline natural gas from somewhere.