Gasoline prices (per AAA) remained flat from last report at $3.574 One year ago the price had ballooned to $4.671

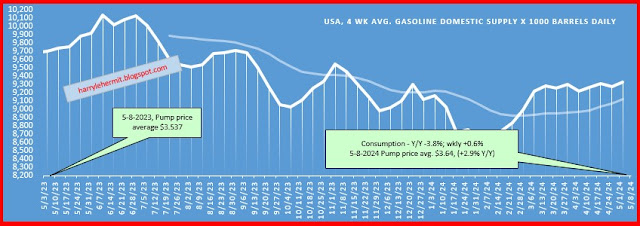

Consumption increased +1.3% from last week, and stands 3.3% above year ago numbers. (This is a four week moving average).

The import/export surplus of gasoline since last March 1st 2022, stands at +99.7M barrels. The import/export numbers have really not changed that much over the past few weeks and this past week showed more exports than imports, by +118K daily.

Where will pump prices be next week? The crack spread is easing and the range appears biased to the downside. My estimate last week was +6.6¢ and was flat, so this week, I am guessing a downside of about -4.7¢. Here's hoping I continue to overestimate the pump price.