With the PCE index report this morning, we can wrap up all the March inflation numbers. Granted, some slight improvement was seen in some areas, but still double digit increases on the upstream models seem to suggest more inflation to the consumer.

As mentioned last month, the core seems to be decelerating and the potential for further decreases appear on the horizon. A lot depends on China's current covid lockdowns and impact on the supply chain.

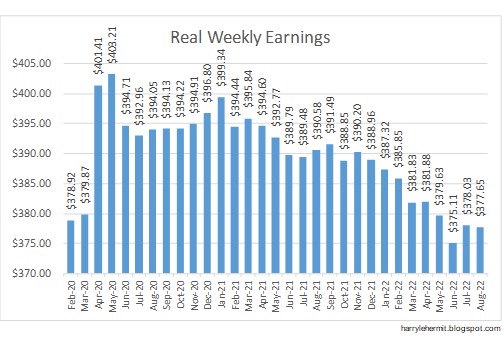

We also see the personal income and outlays for March. Note the current dollars and chained dollars. Chained dollars are only used in a couple of categories. So thrown in inflation and the numbers aren't exactly rosy.

Yesterday the GDP Advance 2022 1st quarter was released and failed to live up to expectations. Quite a bit was made about Consumers still lifting the economy and the trade gap really stifling the numbers. As for the consumers, the bulk of that lift was in the service sector as the goods sector was flat. The Services was up 1.0% quarter to quarter and the trade gap was down 1.4% quarter to quarter. Outside of those two, everything else was tepid, imo. Although Non-Residential Fixed Investment was 2.2% above previous quarter.

One quarter does not a recession make, so the numbers could significantly change as more data becomes available.

Of course, the books are now closing for March, and it is on to April numbers. So, the impact of China's covid shutdown policies will become evident real soon, the "official" impact won't begin to be known until June.

As for consumer inflation for April, I would tend to believe that energy would be flat from March. Don't be misled, as gasoline appears to be edging up at this writing as well as Natural Gas. Core inflation might be decelerating a bit, but food does not appear to be decelerating. Overall, the CPI should "cool" to near 8.0%. Welcome to the late 70s and early 80s of last century.

The U.S. should once again become a net exporter, for the year, of Petroleum and Petroleum Products over the next few weeks, as the exports have ballooned to nearly a 1-million-barrel net exports on a daily average. That million-barrel daily release from the SPR is slated to begin May 1st.

Oh well, this is "fun" times we live in!

Other Stuff...

It amazes me in this day and age... how utterly devoid of knowledge, we Americans have become. Although I can find numerous instances where we are not alone in knowledge deficit.

A near direct quote "Our politicians are always promising to fund infrastructure, yet here we are in 2022 and they have done nothing", which is greeted with broad agreement. Apparently we must all forget Congress passing a $1.4 Trillion infrastructure bill and the President signing it on November 15, 2021.

Usually during this conversation, someone will mention that Trillion Dollar shovel ready infrastructure bill signed by Obama in 2009... and ask what ever happened to that? It never existed. There was a $787 billion stimulus bill, which included about $98 billion for infrastructure, of which a portion was for shovel ready.

We have become equally adept at ignoring stuff that happens and making up stuff that didn't happen.

There really is no hope, so why bother? Everyone slows down to see a car crash or a train wreck or any number of other such things.