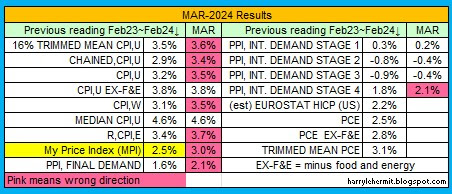

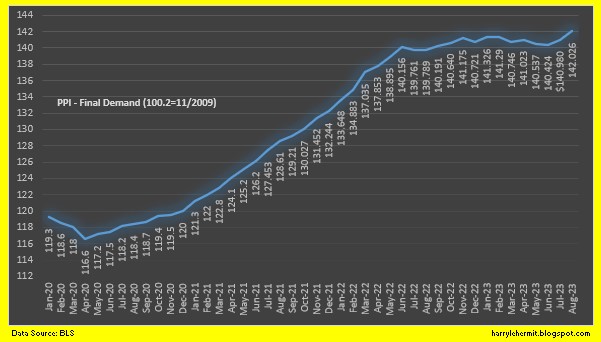

The Producer Price Index was released this morning and indicated an upturn.

Note that I did not revise the December, 2024 final demand, as did the BLS. Yes, December was revised upward to 3.5%. https://www.bls.gov/news.release/archives/ppi_01142025.htm

The nervous nellies will scream inflation is roaring back. Maybe so, but it will not repeat the horrors of 2021~2022. How can I say that? Once you understand the causes, the answer becomes easy.

- After the covid shutdown and collapse of international trade, the shipping industry was in disarray, with containers to move goods... in all the wrong places.

- Retailers had significantly reduced inventories to meet the slowing demand.

- There was a rather large stimulus paid to American citizens, on top of some previous payouts.

- The covid vaccine was becoming rapidly available.

- The American people were told that it was now safe to resume normal activities.

- An impending west coast port strike for mid 2022, which did not materialize.

Newly freed from fear Americans started immediately spending that stimulus money, which boosted retail sales by 10% in the first month. The retailers, started ramping up orders significantly to restock the shelves, which exposed the problems with the shipping containers. This was compounded by retailers, pulling orders well ahead to heavily stock up... prior to the threatened west coast port strike.

The shipping industry has finally recovered, the retail inventories have reached stability, and there are no strike threats on the horizon. There was consideration of a possible port strike on the east coast and gulf, which did increase orders, as well as impending tariff expectations, which also increased orders.

The port strike is in the rear view mirror and the shipping industry sailed through it easily. The tariff question is still to be answered.

As a further note on retail sales... when adjusted for inflation, they have remained at that March, 2021 level. That will likely be the indicator of future demand... or lack thereof.

Tariffs would likely weaken demand, so the expectation of massive inflation due to tariffs... not so much.

{kind=link}