The BLS has released the February Producer Price Index Report. (historical releases)

The Producer Price Index for Final Demand decreased 0.1 percent in February, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. Final demand prices advanced 0.3 percent in January and declined 0.2 percent in December 2022. (See table A.) On an unadjusted basis, the final demand index rose 4.6 percent for the 12 months ended in February.

In February, the decline in the final demand index was led by prices for final demand goods, which fell 0.2 percent. The index for final demand services edged down 0.1 percent.

The index for final demand less foods, energy, and trade services increased 0.2 percent in February after rising 0.5 percent in January. For the 12 months ended in February, prices for final demand less foods, energy, and trade services advanced 4.4 percent.

Final demand goods: The index for final demand goods fell 0.2 percent in February following a 1.2-percent advance in January. A 2.2-percent decline in prices for final demand foods was a major factor in the February decrease. The index for final demand energy moved down 0.2 percent. In contrast, prices for final demand goods less foods and energy rose 0.3 percent.

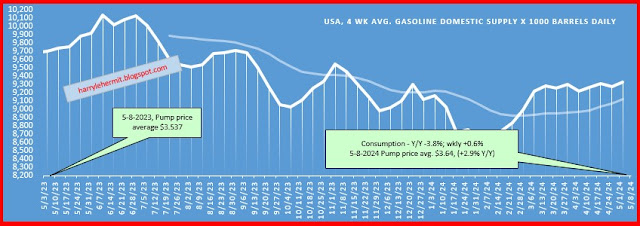

|

| Click image to enlarge |

Okay, so let me blow my horn a bit, with last month's prediction...

Next month is likely to surprise to the low side, possibly even a monthly negative, with annual at the +4.4% range.

Okay, got that out of the way. All in all a good report, with many areas of hope. Now on to the "Nonfood materials less energy." Which, I guess, is similar to core... being without food and energy. That popped +1.2% for the month, following January's +1.6%. I get this feeling it will be near +1.8%, when March's numbers come out.

Still, I would anticipate March to be year over year of +3.0%, and month to month being flat.