Today's EIA.gov report.

Crude stocks grew, +597K barrels, from last week, although still at +1.0% above the 5 year seasonal average. It should be noted the 5 year average includes the abnormal 2020 and 2021 number. Otherwise, the current inventory is nearly +6.0% above normal.

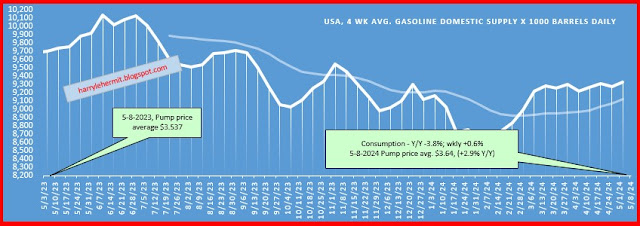

Distillates fell -606K Barrels; and Gasoline slid another -330K barrels. The SPR fell -1.6M barrels.

WTI has risen to $83.21, compared to $80.54, one week ago, and $99.40, one year ago. OPEC + did announce substantial output cuts, but the when, where and who, remains to be seen. The price jump is basically an expectation of China's economy regaining footing.

Refinery output edged up on a weekly basis, but still below one year ago levels. I would make an assumption that the lag is due to refinery maintenance.

For anyone interested, the U.S. has exported 591.9M barrels of crude and petroleum products, more than imported, since March 1, 2022. 1.4M barrels this past week, which is well below previous weeks. It appears to be in crude exports being abnormally low. Maybe a tanker didn't sail on time?

Overall, crude stocks remain quite healthy, compared to this time last year, with days supply at 30.2, compared to last year's 26.7 days.

While crude inventories remain in decent shape, the refining part of the equation is still lagging, compared to one year ago.

I am, also, puzzled by the gasoline side, as importing more than exporting... is somewhat of an anomaly.

{kind=link}