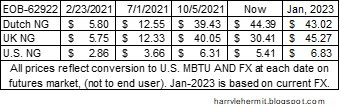

I guess it is no surprise that pump prices are rapidly rising... now standing at 11.5% above year ago levels.

How high could it go? That gets very complicated and depends on...

Past crude oil disruptions

Nothing really compares to the current situation. The 1973 Arab Embargo, targeted the U.S. and a few other countries, which were mostly unaffected. Notably, the U.S. experienced shortages and significant price hikes. The 1980 Iranian revolution impacted the global prices, but not the Straits of Hormuz. Again this impacted the U.S. with spot shortages and sharp price rises.

That latter crisis did result in our current spot pricing structure, which ensures inventory across the different regions of the country.

The duration of closure of the Straits of Hormuz.

This is the determinant of future crude prices, natural gas prices, etc. As these are global commodities, the U.S. is not immune, as a net exporter of crude and LNG.

The 2nd part of the puzzle is shipping costs, which are usually included in those futures pricing. There are a lot of tankers, fully loaded and sitting stationary in that Gulf. Additionally, tankers are starting to pile up at the entrance into the Gulf. All those tankers are basically removing shipping capacity from the equation.

We can all remember the high prices at the pump in 2008, which was caused by a much weaker dollar AND limited transport capability, due to our extreme dependence on imports at that time.

Some basic math.

Currently about 20 million barrels of crude passes through the Straits of Hormuz, each every day. Of that, less than 1 million barrels is shipped to the U.S. 3 million barrels are from Iran and generally goes to China. That leaves 16 million barrels for the rest.

The bulk of U.S. Imports are from Canada, which is largely captive by their government policies and is therefore highly dependant on the U.S. importing their product.

Certainly U.S. exports can rise, but a dramatic uptick in shipping would be hard to achieve, imo. U.S. Pump prices will most certainly rise, dependant upon duration of Straits of Hormuz closure, but there should be no shortages at the pump for at least 3 months. That might not be the case in other countries.

Other overlooked factors

Deducting the 3mbpd exported by Iran to China, there remains 17mbpd of crude not passing through the Straits of Hormuz. That is approximately $1.3B per day of lost revenue to the exporters in that area.

With no ships entering the Straits of Hormuz, countries that are heavily dependent on food imports will experience possible sharp rises in prices, as well as potential shortages.

Summary

As someone that drives very little, an extreme jump in pump prices can be absorbed. As natural gas is a factor in electricity prices, I would expect an uncomfortable jump in that. With diesel prices jumping faster than gasoline and reliance on transportation of products... it will increase things I use on a regular basis.

For me... inflation is the story, NOT shortages, unless it would be shortage of money.