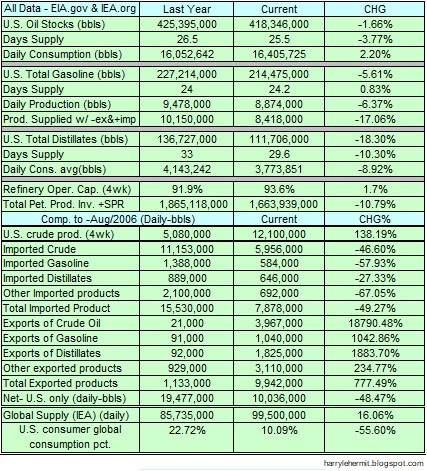

The EIA released the latest weekly report, and there is a continuing sliver of demand destruction. The numbers do seem to suggest it, with the day's supply of 24.1 from last week jumping up to 24.5 on this week's report.

Gasoline Inventories rose 333K barrels from last week. This is spite of exports being 1M Bbl. more than imports.

The market for gasoline is still declining, and looks to continue with this report. According the the AAA, the national average has slipped 7.8¢ from last week, and my guess... there is room for another 56¢, although weather may become an obstacle at this point.

Speaking of weather, the models aren't showing anything of T.S. variety hitting the U.S. East or Gulf Coasts out to the 3rd week of September. Keeping fingers crossed.

Crude stocks increase 8.8M BBLS from last week and exports of crude and petroleum products outpaced imports by 4.8M BBLS. WTI is down about $3.50 from last week. Basically, back to End of January numbers. Of course, there is some rumbling of OPEC+ slashing production by 1M barrels per day, as well as suggestions of further SPR releases.

Diesel fuel continues to be problematic in some areas...

|

| Click to Enlarge |

For the rest of the picture...

|

| Click to Enlarge |

This is likely my last weekly review of the report. I will continue to track, but blogging about it has become somewhat tiresome. I see what I see and understand what I see, but conveying those thoughts in a coherent manner is the issue.