The EIA.GOV released their weekly report.

Here are some interesting tidbits... Our exports of Crude and Petroleum Products since March, stands at 124,758,000 million barrels more than our imports, which up near 5 million barrels from last week's report. Gasoline exports during the same period now stands at 16,625,000 million barrels more than our imports and up about 400K from last week.

There is some semblance of relief at the pump, as current conditions indicate the national average drifting lower another 50¢ to around $4.25. You would think they might be lower, with demand decreasing, but imports still rule the day. If and when Europe settles down, expect these high prices to continue. But hooray, we can cheer for $4.25 at the pump, like it is some sort of consumer victory.

As certain politicians are already cheering the SPR release as working. It kept the crude prices somewhat at bay, but really did nothing for gasoline prices in the USA. You simply cannot export gasoline like we have the past 4 months and expect anything different.

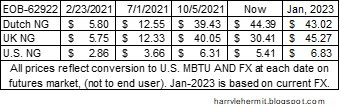

Now on to natural gas (data from yesterday's close)...

I cannot help but notice the problems with futures, concerning U.K. and Europe in general. I recognize that U.K and Europe are outside my area of concern, but we talk about recession in the USA and what we are doing or not doing (about it), when we might consider a recession in U.K. and Europe, despite what they are doing or not doing.

I wouldn't count out a NG shortage this winter in Europe. It would serve you know who quite well, as it would divide NATO. You know who might get blamed for a cutoff, but the root blame would fall elsewhere and by elsewhere... you know where!

On the bright side, the gasoline prices in the U.S. should continue to fall, as no hurricanes or "other" storms appear on the horizon. Even U.S. natural gas has somewhat stabilized, due to Freeport shutdown.

Amazingly, government regulators have stepped in to embark on strenuous safety oversight... which will likely delay Freeport's timetable for restart and full operation of LNG exports. Remember... it is all about safety and has nothing to do with replenishing U.S. natural gas storage for the coming winter.