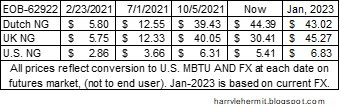

How

did we get where we are?

In

previous postings, I made mention of the repeal of the Crude Export Act in 2015. That set the stage for

exporting of crude from the U.S., which was due in part to drill baby drill and

lowering of WTI prices within the U.S. As a result, ALL crude oil became priced on the

global market demand. At that time, exports were limited to Alaskan Crude and

daily exports were in the 500K barrel range.

Also at

that time, WTI crude had fallen to $34.74 per barrel and gasoline stood at

$2.026 per gallon nationally. This was down from the high of $100+ per

barrel in July of 2014, as was gasoline at $3.60+ per gallon. Which was prior

to drill baby drill taking hold. Hence the necessity to do something for the

drillers.

In

February 2020, WTI crude had risen to $51.43 and gasoline to $2.466. Exports of

Crude were in the 3.5M barrels daily.

Of

course, February 2020 gave us the first glimpse of COVID. With Covid the infamous

negative futures price of -$37.63 in April (Monthly average at $17.13). People

were paying someone else to take delivery of crude. Gasoline fell to $1.773 by

end of April. Crude exports slowed to the 3M barrel daily level.

[All

data from EIA.GOV]

The

crude prices stayed in the $40 range until December 2020 and gasoline in the

$2.20 range. It was about this time that an antsy public was given hope via

vaccines. By February 2021, crude was in the $60 range and gasoline had jumped

to $2.60+.

While

there had been spot shortages of many goods early on, they had mostly eased by

this time, as well. There were lingering shortages of materials to repair

equipment, build cars, etc. The economy was still out of balance, in my

opinion.

As

the shots became widely available and hopes of finally ridding covid seemed on

the horizon... consumers became increasingly anxious to get out of lockdowns,

etc.

The

economy had largely survived due to stimulus. It was in February that Texas had

the big freeze, with impacted refining and saw gasoline jump to $2.80

range.

Then

came the 3rd stimulus, which even Miss Transitory thinks was too much... in

retrospect.

It is nearly impossible to avoid what happened next, as the American Consumer went all in on a spending spree. This resulted in port backups, intermodal congestion and Just in Case inventory. Which in turn resulted in this...

Crude also began its climb, as

demand increased. By end of 2021, it was nearing $80 and gasoline was in the

$3.30 range. We were still exporting around 3M barrels per day. Even with the

shuttering of older refineries. Why spend money on something that is being

phased out, due to climate change?

Then came Ukraine and the

recognition that Europe is dependent upon Russia. Before the invasion, Crude

had already climbed to $92 and gasoline to $3.60.

Interestingly, certain politicians

have advocated assisting Europe wean itself from Russian energy. Even an age-old

enemy such as Venezuela is now somehow to be considered friendly. An old friend

(Saudi Arabia) that became NO longer a friend, is now to be once again...

viewed favorably.

We are now exporting 3.5M barrels on

average per day since March and some days goes above 4 million. And it's not

just crude, but refined products as well. 102,309,000 barrels of crude

and petroleum exports ABOVE what has been imported since first of March. Oh and

14,091,000 barrels of gasoline have been exported in that period, ABOVE

imports.

Here is how it has flipped since this period in 2019...

I have highlighted the flip areas.

Where once we imported more of all products, than we exported AND where we once

imported more gasoline than we exported.

In my opinion, we would still be

seeing record prices at the pump, although not in the $5 range (certainly above

$4 and still be complaining). So, it would be correct to blame the current

prices on Putin, but to run around suddenly buddying up some folks, releasing

SPR to the tune of 1M barrels a day, then complain about refineries doing what

you asked, is a bit much. I am not defending refineries, just noting the

hypocrisy of certain politicians.

What's next... blaming the high

prices on climate change? We are just one hurricane in the Gulf from the blame

game to shift to that very item. I also found the timing of blaming refineries,

just as he or his henchmen got advance news of impending bad economic reports.

Those bad economic reports have caused the futures of both crude and gasoline

to fall nearly 10% this past week.

I'm sure the subsequent fall in pump

prices will be extolled as proof the refineries were gouging us. And many

Americans will believe it, report it, etc. One reporter noted that we consumed

10% more gasoline this past week than the previous week, although the data says

-1.0% for the week and -2.9% year over year. Seriously, are we that ignorant,

not to see through these lies? Apparently, the answer is yes.

Which brings me to the IQ of the

American people. On certain social media boards, there are still individuals

saying we should drill more, etc. without regard to the fact we are exporting.

Some people haven't gotten the news or are ignoring it for political

gain.

Of course, the thread that caught my

eye, was regarding the falling IQ of Americans. According to one individual,

the IQ of Americans was once 110 and has now fallen to 99 and is a clear

indication of our stupidity. That no one pointed out the obvious flaw and piled

on to that belief... does indicate our stupidity. I doubt anyone caught the irony

of the original post, including the original poster.

I consider myself of average

intelligence and possibly with age... below. It is kind of scary to think where

we are headed.

#gasoline #covid #crude-oil #alaska #opinion #exports