The real GDP for the 2nd Quarter was released and it was below forecasts. I think it was generally in the 0.8% annualized. My pathetic attempt was 0.6% annualized. The result was -0.9%. The pundits have fixated on the falling inventories, but I noticed the imports/exports did not match expectations.

The consumer was steadfast in increasing spending, but slowly. (Did I mention real GDP is after adjusting for inflation?)

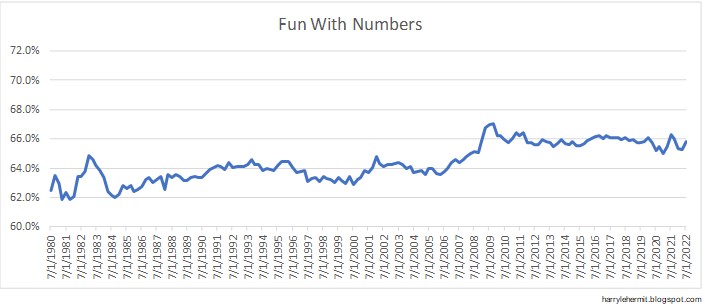

Here is a bit of history for consumer spending relative to real GDP.

While the consumer edged up, and some gains in net export, Gross Private Domestic Investment was the big drag, it was the inventory numbers that pulled it down by $107B from last quarter. That was the surprise for many people and the difference between the result and what was forecast.

Then we have Personal Income and Outlays, which...

Personal income increased $133.5 billion (0.6 percent) in June, according to estimates released today by the Bureau of Economic Analysis (tables 3 and 5). Disposable personal income (DPI) increased $120.4 billion (0.7 percent) and personal consumption expenditures (PCE) increased $181.1 billion (1.1 percent).The PCE price index increased 1.0 percent. Excluding food and energy, the PCE price index increased 0.6 percent (table 9). Real DPI decreased 0.3 percent in June and real PCE increased 0.1 percent; goods increased 0.1 percent and services increased 0.1 percent (tables 5 and 7). (emphasis added)

Even with disposable income sliding after inflation adjustments, the consumption increased after inflation adjustments. Borrowing?

Then the various inflation numbers...

Not much to be enthusiastic about. It would appear that some of the forecasts are starting to downgrade inflation number for July and I would tend to agree. At best it would seem to have peaked.

As to whether we are in a recession or not... the idea of "technical" recession is an imported idea. The U.S. has never jumped on the 2 quarter as recession bandwagon. Harken back to the Great Recession. It was deemed the U.S. started into recession in December 2007, yet we did not have back to back negative GDP, until 3rd and 4th quarter 2008.

I would think we are likely heading into a recession, but not at the moment. Then the issue is how long and how deep?

So good luck and on to next month's data.