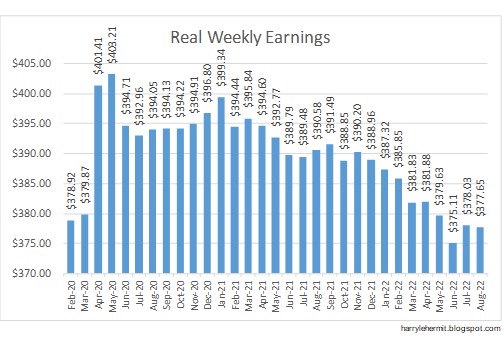

The BEA released the Personal Income and Outlays, August 2022 and Annual Update this morning.

|

| Click to Enlarge |

|

| Click to Enlarge |

Real gross domestic income (GDI) increased 0.1 percent in the second quarter, a downward revision of 1.3 percentage points from the previous estimate. The average of real GDP and real GDI, a supplemental measure of U.S. economic activity that equally weights GDP and GDI, decreased 0.3 percent in the second quarter, a downward revision of 0.7 percentage point (table 1).

|

| Click to Enlarge |

The standard monthly premium for Medicare Part B enrollees will be $164.90 for 2023, a decrease of $5.20 from $170.10 in 2022. The annual deductible for all Medicare Part B beneficiaries is $226 in 2023, a decrease of $7 from the annual deductible of $233 in 2022.

It is unusual the announcement could be made so early, as it usually comes in mid November, which always fall just after an election. The announcement is barely visible on all those old people boards I follow. It's still good to be able to keep and additional $62.40 per year, even if it would purchase what was $57.35 last year.

Speaking of inflation, the September numbers from the BLS will come out on the 13th of October. Here is my current projection of C.O.L.A.

|

| Click to Enlarge |

I'm struggling on whether it will be 8.7% or 8.8%. Earlier, I had 8.6% in the mix, but I think that has gone bye bye. Likely 8.8%, with a possible 8.9%.

Frankly, the likelihood of the CPI-U jumping 0.28% and the CPI-W at 0.37% is not unreasonable, although something a bit lower on the CPI-W lands at 8.8%.

In July, the -7.7% drop in gasoline covered up all the other price inflation taking place. In August, the -10% drop in gasoline could NOT cover up all the other price inflation taking place. September is ending with only a -5.5% drop in gasoline. So look out.

Much of the reason for the national average of gasoline prices rising the past ten days, has to do with California switching from summer blend to winter blend. It happens every year. It should begin slowing next week.

Most Americans don't grasp that, but politicians do. So a wonderful time to point out the national average is rising, proclaim retailers must halt the exploitation and then take a victory lap next week. We Americans are such suckers.

As for gasoline prices, I am not sure what they will do, when that 1MBPD SPR release ends just before the election. Couple that with the possibility of OPEC cutting a few barrels... who knows.

Natural Gas is staying ahead of the curve and possibly gaining some...

|

| click to enlarge |

All in all, another decent month. It could be the last for awhile, but who knows? Or rather... who cares?

|

| Click to Enlarge |