Time for more painful inflationary discussion. The BLS has now released the July Report. (historical releases)

The basic graph...

Yeehaw!! We finally have a negative number -0.5%... the first since March, 2020. We can jump for joy, as the inflation peak is finally here. Or is it?

Maybe not, if you like to do certain things... like eat. Food +1.0% M/M and +15% Y/Y. Of course, we shouldn't put all our eggs in one basket, although eggs up are +44.2% for the month and 171.5% for the past year. Maybe one egg is all you can afford. Can you even afford the basket?

After a slowdown in beef and veal and some easing of pricing at both the CPI and PPI... guess what? Down -4.4% since last year, but up 9.5% for the month!! Maybe time for the other "white" meat, as pork continues to slip, -0.5% for the month and -7.7% annual. Maybe some chicken, as well.

BTW, foods are largely weather dependent and in case you haven't noticed... hot weather + prolonged dry conditions, will impact food going forward. Even a change in diet will be hard to escape inflation, in my humble opinion. Food is a basic necessity.

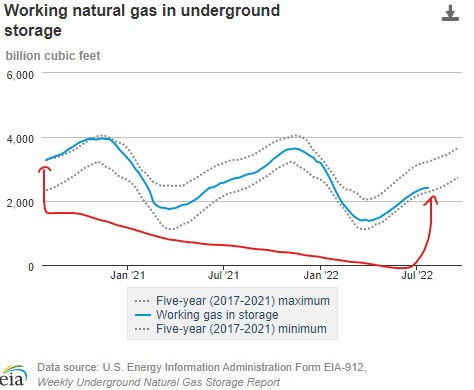

Energy seems to be falling, but step away from gasoline for a moment and you realize that Electricity is rising and although Natural Gas slipped last month, expect a rebound going forward. The futures market says so.

Overall, energy is more about geo-political issues and demand/supply. Supply in some areas will continue to falter, while demand in others may slip.

For the month...

- All items, -0.5%

- Food, +1.0%

- Energy, -9.0%

- All items less food and energy, +0.2%

- All items, +9.8%

- Food, +15.0%

- Energy. +36.8%

- All items less food and energy, 8.5%

There are many nuggets of information in the report, to fit whatever bias you may have.

The current state of July reports and releases (as always, the Eurostat/USA figure is my concoction based on the Eurostat formula)...

The upstream numbers are decreasing, but with PPI final demand at 9.8% and the CPI-U at 8.5%... I don't think inflation is quite done with us.

While you are enjoying your roasted coffee (-2.3% from June), please explain why corporate media is avoiding much discussion of this PPI release?😞